| Forecast Period | 2024-2028 |

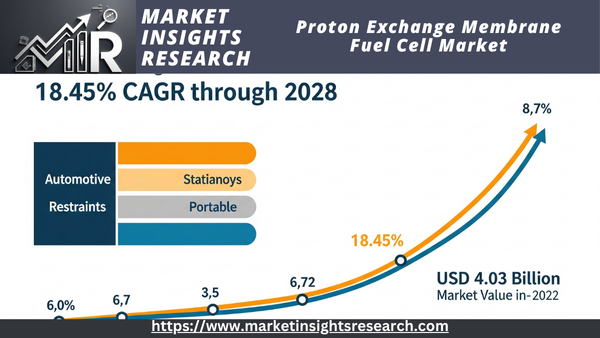

| Market Size (2022) | USD 4.03 billion |

| CAGR (2023-2028) | 18.45% |

| Fastest Growing Segment | High Temperature |

| Largest Market | North America |

Market Overview

Global Proton Exchange Membrane Fuel Cell Market has experienced tremendous growth recently and is poised to continue its strong expansion. The Proton Exchange Membrane Fuel Cell Market reached a value of USD 4.03 billion in 2022 and is projected to maintain a compound annual growth rate of 18.45% through 2028.

Download Free Sample Ask for Discount Request Customization

Key Market Drivers

Growing Environmental Concerns and Carbon Emission Reduction

Growing environmental consciousness and the pressing need to cut carbon emissions are major factors driving the global proton exchange membrane fuel cell (PEMFC) market. This urgent problem has sparked a significant global change in the ways that energy is generated and consumed, and PEMFCs are now a well-known way to lessen the negative effects of conventional fossil fuel-based energy sources.

Air pollution, climate change, and the depletion of finite fossil fuel supplies are just a few of the pressing environmental issues. The catastrophic effects of global warming, such as extreme weather events, rising sea levels, and ecosystem disruptions, have been repeatedly warned about by climate scientists and experts. As a result, there is growing international agreement that switching to cleaner, more sustainable energy sources is essential. PEMFCs provide an appealing solution to these environmental issues because of their exceptional capacity to generate electricity via an electrochemical process utilizing hydrogen and oxygen. PEMFCs only emit water vapor as a byproduct, producing no harmful emissions in contrast to traditional combustion-based energy sources. This essential quality fits in well with the need to lower greenhouse gas emissions and carbon footprints, which are the main causes of climate change.

The necessity of achieving significant reductions in carbon emissions has been embraced by governments, international organizations, and environmental advocates. For example, the Paris Agreement is a worldwide pledge to keep global warming well below 2 degrees Celsius over pre-industrial levels. Rapidly switching to low-carbon and carbon-neutral energy sources is necessary to meet this goal, and PEMFCs are essential to this shift.

The use of PEMFCs in fuel cell electric vehicles (FCEVs) is causing a major shift in the transportation industry, which contributes significantly to carbon emissions. FCEVs are zero-emission cars that use PEMFCs to turn hydrogen into electricity so that the electric motor can run. FCEVs are becoming more popular as a sustainable substitute for internal combustion engine vehicles as automakers and governments around the world place a higher priority on lowering transportation-related emissions. PEMFCs make it possible for FCEVs to provide long driving ranges, quick refueling times, and a clean driving experience, which makes them a practical way to lower carbon emissions in the transportation industry.

Additionally, PEMFCs are being used more and more by businesses, residential areas, and commercial buildings for backup power and distributed power generation. PEMFC systems are a desirable option for clean energy generation due to their capacity to function effectively with low emissions. This enhances energy resilience and dependability while also lessening the environmental effect of energy production.

Investments and incentives for the creation and application of PEMFC technologies are being driven by the increased awareness of environmental issues. Governments and private sector entities are investing heavily in research, development, and infrastructure to support the adoption of PEMFCs. Incentives such as grants, tax credits, and subsidies are being offered to accelerate the deployment of PEMFC systems in various applications, from transportation to stationary power generation.

In conclusion, growing environmental concerns and the need to lower carbon emissions are driving significant growth in the global proton exchange membrane fuel cell (PEMFC) market. PEMFCs represent a clean, efficient, and versatile energy solution that aligns with global efforts to combat climate change and transition to a more sustainable energy future. As the world strives to achieve ambitious carbon reduction goals, PEMFCs are poised to play an increasingly integral role in decarbonizing various sectors and advancing environmental sustainability.

Energy Security and Decentralization

Two key elements driving the global market for proton exchange membrane fuel cells (PEMFCs) in a positive direction are energy security and decentralization. PEMFCs have become a ground-breaking solution in a time when worries about environmental degradation, the depletion of fossil fuels, and the requirement for resilient energy systems are growing.

First of all, countries all over the world now prioritize energy security. Because they mostly depend on fossil fuels, traditional energy sources are vulnerable to supply disruptions, price volatility, and geopolitical tensions. The need to diversify energy sources and build resilient energy infrastructures has become increasingly apparent as a result of these vulnerabilities. Hydrogen-powered PEMFCs present a strong substitute. There are several ways to produce hydrogen, such as gasification of biomass, reforming of natural gas, or electrolysis of water. By lowering reliance on a single energy source or supplier, this versatility in hydrogen production improves energy security. Furthermore, hydrogen has a long storage life, making it a useful safeguard against interruptions in the energy supply. Given that natural disasters and geopolitical conflicts have the potential to disrupt traditional energy supply chains, this feature is especially crucial. PEMFCs are becoming more widely acknowledged as a crucial component of energy independence as governments and businesses place a higher priority on energy security. Second, the global energy landscape is being reshaped by the revolutionary trend of decentralization. Conventional centralized systems for power generation and distribution are frequently ineffective, vulnerable to transmission losses, and less flexible in response to the evolving energy environment. PEMFCs, on the other hand, provide a decentralized method of producing energy. From tiny residential units to larger industrial applications, these fuel cells can be used at different scales. They can even be incorporated into transportation systems, such as fuel cell vehicles. By empowering people, companies, and communities to generate their own clean energy, decentralization lessens their dependency on centralized utilities. It also enables the integration of renewable energy sources like wind and solar power, with excess electricity used to produce hydrogen for PEMFCs. This synergy between renewable energy and PEMFCs promotes sustainability and resilience by decreasing greenhouse gas emissions and enhancing energy reliability.

Furthermore, the decentralized nature of PEMFCs supports grid resilience. In the event of power outages or disasters, local PEMFC systems can continue to provide electricity, heat, and even potable water, ensuring critical services remain operational. This resilience is especially useful in places that frequently experience severe weather or in isolated locations with little access to dependable electricity.

In summary, the need for decentralization and energy security is driving the global proton exchange membrane fuel cell market. PEMFCs have become a flexible and sustainable solution as the world looks to lessen its reliance on fossil fuels, slow down climate change, and improve energy resilience. Their capacity to diversify energy sources, facilitate decentralized energy generation, and generate clean energy from hydrogen is a perfect fit with the changing energy landscape. The need for PEMFCs is expected to increase as governments, businesses, and communities place a greater emphasis on these objectives. This will spur innovation and change in the energy sector and help ensure a more secure and sustainable energy future.

Download Free Sample Ask for Discount Request Customization

Advancements in Hydrogen Infrastructure and Renewable Hydrogen Production

Two key factors driving the global proton exchange membrane fuel cell (PEMFC) market are the growth of renewable hydrogen production and advancements in hydrogen infrastructure. These developments are transforming the energy landscape and bolstering the adoption of PEMFCs as a versatile and sustainable energy source.

First off, the growth and improvement of hydrogen infrastructure is a key driver of the PEMFC market. Hydrogen infrastructure encompasses the entire supply chain, from production and storage to distribution and transportation. Historically, one of the challenges impeding the widespread adoption of PEMFCs has been the lack of hydrogen refueling stations and distribution networks. However, significant strides have recently been made to address this problem. Governments and private sector organizations have made significant investments in developing hydrogen infrastructure, particularly in regions with aggressive hydrogen strategies like Europe, Japan, and parts of North America.

Two examples of this expansion that will increase the effectiveness of delivering hydrogen to end users are the development of hydrogen refueling stations for fuel cell vehicles and the integration of hydrogen into existing natural gas pipelines. Building hydrogen production facilities, such as electrolyzers powered by renewable energy sources, also contributes to a cleaner and more sustainable hydrogen supply chain. By lowering the barriers to entry, the expansion of this infrastructure makes PEMFC more accessible to consumers and businesses alike.

Second, the increasing focus on generating hydrogen from renewable sources is a major driver of the PEMFC market. Renewable hydrogen is produced by electrolysis, which splits water into hydrogen and oxygen using electricity from renewable sources like solar or wind. With hydrogen-based technologies like PEMFCs, this emission-free hydrogen production method holds great promise for addressing sustainability concerns.

The global push to decarbonize and transition to cleaner energy sources is ideally suited to the growth of hydrogen production from renewable sources. PEMFCs profit greatly from this trend since using renewable hydrogen as a fuel source significantly reduces the carbon footprint of fuel cell applications. This shift to cleaner hydrogen production not only enhances PEMFCs' environmental credentials but also aligns them with stringent emissions reduction targets set by governments and corporations.

Furthermore, the use of renewable hydrogen in PEMFCs promotes energy resilience and dependability. PEMFCs powered by renewable hydrogen can be used as distributed energy systems, serving as a backup power source in the event of a grid outage and a dependable energy source for critical infrastructure. This capability not only increases grid resilience but also strengthens the security and resilience of the energy ecosystem.

In conclusion, the primary drivers of the global market for proton exchange membrane fuel cells are the expansion of renewable hydrogen production and advancements in hydrogen infrastructure. These developments are fostering a more accessible, sustainable, and ecologically friendly PEMFC ecosystem. The logistics of adoption are made easier by the development of hydrogen infrastructure, and the global transition to cleaner energy sources is aided by the growing supply of renewable hydrogen. As long as governments and corporations continue to invest in these technologies and infrastructure, PEMFCs' potential as a clean and flexible energy source is expected to increase dramatically, contributing to the development of a more resilient and sustainable energy future.

Key Market Challenges

Cost and Scalability

The growing need for efficient and clean energy solutions has been the main driver of the Proton Exchange Membrane Fuel Cell (PEMFC) market's steady growth in recent years. But like any emerging sector, it has its share of difficulties, with cost and scalability being the two main ones. In the PEMFC market, cost is arguably the biggest obstacle. PEMFC technology has historically been linked to high production costs, despite its great potential for a variety of uses, such as stationary power generation and transportation. One major obstacle to broad adoption has been the expense of producing essential parts like the bipolar plates, catalysts, and proton exchange membrane. These parts frequently call for pricey materials, complex production procedures, and strict quality control procedures. Costs have also increased as a result of the restricted supply of some essential materials, like platinum for catalysts. Because of this, PEMFC systems continue to be too costly for a large number of prospective users and applications.

For the PEMFC market to continue growing, the cost issue must be resolved. The goal of research and development has been to identify substitute, affordable materials and production processes. There is hope that advancements in membrane materials, manufacturing techniques, and catalyst design will lower production costs. Economies of scale can also be very important for cutting costs. The cost per unit is anticipated to drop as the industry expands and production volumes rise, making PEMFC systems more competitive with traditional energy sources.

Another significant issue facing the PEMFC market is scalability. PEMFC technology has proven successful in specialized applications like backup power systems and forklifts, but it is still difficult and intimidating to scale up to meet the needs of larger applications like passenger cars or grid-scale power generation. Maintaining durability and performance as the fuel cell stack grows in size is one of the main scalability challenges. The efficiency and dependability of larger stacks may be adversely affected by temperature fluctuations, problems with gas distribution, and mechanical stresses. Furthermore, there are scalability issues with the infrastructure needed to facilitate the broad use of PEMFC technology. To meet the growing demand for hydrogen fuel, networks for hydrogen production, storage, and distribution must be established and extended. For example, setting up refueling stations for cars that run on hydrogen necessitates large financial outlays and cooperation from several parties. PEMFC technology's quick scalability may be hampered by this expensive and time-consuming infrastructure development process.

Industry participants are working with governmental organizations and academic institutions to create thorough infrastructure deployment roadmaps in order to address the scalability issue. The smooth transition to a larger scale requires regulatory support, research and development investment, and strategic planning. To improve the performance and dependability of large-scale PEMFC systems, improvements in control strategies and system integration are also being sought. In conclusion, the market for proton exchange membrane fuel cells has enormous potential as a clean and effective energy source, but it also faces major obstacles in terms of scalability and cost. Historically, high production costs have prevented PEMFC technology from being widely adopted, and overcoming infrastructure and technical obstacles is necessary for PEMFC technology to scale for larger applications. However, a more affordable and scalable PEMFC market is being made possible by coordinated research, development, and cooperation among industry players, governments, and academic institutions. This market has the potential to completely transform the energy landscape and lessen our reliance on fossil fuels.

Hydrogen Infrastructure and Storage

The development of the proton exchange membrane fuel cell (PEMFC) is crucial to its broad use in the global market.A fundamental prerequisite for the success of PEMFC technology is hydrogen infrastructure. Unlike traditional fuels like natural gas or gasoline, hydrogen, the main fuel for PEMFCs, does not have a well-established and extensive infrastructure. This restriction covers the aspects of hydrogen production, distribution, and refueling. There are several ways to produce hydrogen, but expanding the infrastructure and finding effective storage solutions are major obstacles. Even though PEMFC technology has a lot of potential for clean energy solutions, it faces challenges with storage and infrastructure, including biomass gasification, steam methane reforming, and electrolysis. However, if not sourced sustainably, these techniques can lead to greenhouse gas emissions and are frequently energy-intensive. One of the biggest challenges is scaling up hydrogen production in a way that is both economical and environmentally friendly.

Furthermore, there are challenges in getting hydrogen to end users. Because hydrogen has a low energy density per unit volume, it is difficult to transport and store efficiently, which raises transportation costs when compared to traditional fuels. It is possible to convert existing natural gas pipelines to hydrogen, but this will cost a lot of money and require extensive retrofitting. Although they exist, alternative distribution methods like liquid hydrogen tankers and high-pressure tube trailers are costly and necessitate a specialized logistics network. Another urgent issue is the development of a widespread infrastructure for hydrogen refueling. Governments, fuel cell manufacturers, and energy companies are among the many stakeholders who must coordinate and invest heavily in the construction of hydrogen refueling stations (HRS). The expansion of HRS networks has been hampered by the low demand for hydrogen vehicles in many areas. Potential customers might be reluctant to switch to hydrogen-powered cars if there aren't enough refueling stations, which would create a catch-22 situation.

Another barrier to the expansion of the PEMFC market is effective hydrogen storage. Both liquid and gaseous forms of hydrogen storage have benefits and disadvantages. Although it can be safe, storing gases in solid-state materials or high-pressure tanks necessitates large tanks and uses energy during compression. Although liquid hydrogen has a higher energy density, its storage and transportation are complicated by its requirement for cryogenic temperatures. Innovation and research are essential to addressing these issues. The creation of cutting-edge hydrogen storage materials, such as carbon nanotubes, metal hydrides, and chemical hydrogen storage, has the potential to increase storage efficiency. Furthermore, hydrogen storage solutions may undergo a revolution due to developments in solid-state hydrogen storage materials.

In order to overcome infrastructure and storage challenges, policy support is also necessary. By offering financial incentives, expediting the permitting process, and establishing precise guidelines for hydrogen production and emissions, governments and regulatory agencies can encourage the development of HRS networks. The development of hydrogen infrastructure can be harmonized through international agreements and collaborations, enabling the smooth cross-border transfer of hydrogen technologies. In conclusion, the difficulties associated with hydrogen storage and infrastructure pose serious barriers to the expansion of the worldwide market for proton exchange membrane fuel cells. A multifaceted strategy is needed to address these issues, one that includes international cooperation, policy support, and technological advancements in hydrogen production, distribution, and storage. To fully utilize PEMFC technology and make the shift to cleaner, more sustainable energy in the future, these obstacles must be removed.

Download Free Sample Ask for Discount Request Customization

Durability and Lifespan

One of the most important issues facing the global proton exchange membrane fuel cell (PEMFC) market is making sure that these fuel cell systems are long-lasting and durable. A key component that directly affects the PEMFC technology's economic feasibility and broad use in a variety of applications, from stationary power generation to transportation, is durability. PEMFCs have a number of benefits, such as quiet operation, low greenhouse gas emissions, and high energy efficiency. For the technology to realize its full potential, however, major challenges pertaining to lifespan and durability must be overcome. The deterioration of important components over time is one of the main issues with PEMFC durability. A number of variables, including temperature, humidity, and chemical exposure, can cause the proton exchange membrane (PEM), which is essential for enabling the electrochemical reactions inside the fuel cell, to deteriorate. The fuel cell performs worse as the PEM deteriorates, which eventually lowers the fuel cell's efficiency and dependability. Durability may also be impacted by the catalysts used in PEMFCs, which are frequently based on precious metals like platinum. Over time, these catalysts may degrade and lose their activity.

PEMFC longevity and durability are complex issues. Manufacturers and researchers are tackling these problems in a number of ways. The creation of PEM materials that are more resilient and chemically stable is one strategy. To increase the lifespan of fuel cell systems, researchers are looking into advanced PEM materials with better resistance to thermal and chemical degradation. Under challenging operating circumstances, like high temperatures and fluctuating humidity levels, these materials are designed to preserve their integrity and functionality. Another tactic is to use less costly catalysts, such as platinum, or look for more affordable and long-lasting catalyst materials. Fuel cell producers can lower overall costs and increase product lifespan by reducing catalyst degradation. Enhancing durability also heavily depends on advancements in system engineering and design. PEMFC degradation may be exacerbated by problems with temperature swings, water management, and gas crossover that can be lessened with better thermal control, optimized flow fields, and enhanced sealing methods. Furthermore, in order to accurately evaluate the long-term durability of PEMFCs, rigorous testing and accelerated aging protocols are necessary. Manufacturers can find design flaws and areas for improvement by using accelerated stress tests, which can replicate years of operation in a controlled environment. In the automotive industry, where fuel cells must function dependably for the duration of a vehicle's anticipated life, the durability issue is especially important. Gaining the trust of consumers and successfully commercializing fuel cell vehicles depend on meeting strict durability requirements.

Research programs, government initiatives, and industry partnerships are actively fostering improvements in PEMFC durability in order to address these issues. Research and development initiatives aimed at enhancing PEMFC parts, materials, and manufacturing procedures are supported by funding opportunities and public-private partnerships. In conclusion, one of the biggest obstacles facing the global proton exchange membrane fuel cell market is the longevity and durability of PEMFCs. It takes constant innovation in materials, catalysts, system architecture, and testing techniques to meet these challenges. PEMFCs will become more dependable and economical as durability increases, making them a more appealing and sustainable energy option for a range of uses and ultimately helping to create a cleaner and greener future.

Key Market Trends

A number of significant trends that are influencing the direction of this technology have surfaced in the quickly changing global proton exchange membrane fuel cell (PEMFC) market. The increasing interest in hydrogen-based energy sources and the potential of PEMFCs to handle a variety of applications are reflected in these trends. Three noteworthy developments in the worldwide PEMFC market are as follows

The growing variety of applications is one noteworthy trend in the PEMFC market. PEMFCs have historically been mostly linked to automotive applications, like hydrogen fuel cell vehicles (FCVs). But the technology is now making its way into a number of other industries, helping to create a more decentralized and sustainable energy environment.

Even though FCVs are still becoming more popular, particularly in areas like Europe and parts of Asia where there is a focus on lowering emissions, the trend is spreading beyond passenger cars. PEMFC technology is being adopted by commercial vehicles, such as trucks and buses, because it has the potential to provide long driving ranges and rapid refueling, making them appropriate for freight operations and public transportation.

In both residential and commercial settings, PEMFCs are being used more and more for stationary power generation. These devices, also known as micro-CHP (Combined Heat and Power) units or hydrogen fuel cell generators, offer a clean and effective source of heat and electricity. They are being used as distributed energy resources, backup power systems, and even as main power sources for isolated or off-grid areas.

PEMFCs are advancing material handling machinery, including warehouse trucks and forklifts. They are an appealing option for a range of manufacturing and logistics applications due to their capacity to run effectively indoors where emissions are an issue and refuel rapidly.

Trains and ships propelled by hydrogen are becoming a competitive alternative to conventional fossil fuel propulsion. In order to lower greenhouse gas emissions and advance clean transportation in the rail and maritime industries, PEMFCs are being incorporated into locomotives and ships.

PEMFC technology is also becoming more popular in the aerospace sector, where high-energy-density, lightweight power sources are essential. In an effort to lessen aviation's environmental impact, hydrogen fuel cells are being investigated as an auxiliary power source for aircraft.

Segmental Insights

Type Insights

The market for proton exchange membrane fuel cells is dominated by the high temperature segment worldwide. There are several reasons for this dominance, including

High temperatures are the renewable energy source that is expanding the fastest in the world. This is a result of both the growing demand for clean energy and the falling cost of solar panels.

Proton Exchange Membrane Fuel Cells (RECs), which are tradable certificates that reflect the environmental characteristics of renewable energy generation, are in high demand. Businesses and organizations looking to lessen their carbon footprint are drawn to RECs.

Government support for high temperaturesTo encourage the implementation of high temperatures, governments worldwide are offering financial incentives and other types of assistance. The market for high temperatures and the need for RECs are expanding as a result.

The market for proton exchange membrane fuel cells is also expanding significantly in other segments, including gas power, hydroelectric power, and low temperature. For the foreseeable future, High Temperature is anticipated to continue to dominate this market.

The global market for high-temperature proton exchange membrane fuel cells is anticipated to continue expanding quickly in the upcoming years. The High Temperature market's sustained expansion and businesses' and organizations' growing need for RECs will be the main drivers of this growth. Here are some more details about the global proton exchange membrane fuel cell market's high temperature segmentUtility-scale solar and distributed solar are two more subcategories of the High Temperature segment. Large solar projects that are usually grid-connected are known as utility-scale solar projects.

Smaller solar projects that are usually placed on rooftops or on tiny pieces of land are known as distributed solar projects.

RECs can be produced by distributed solar projects as well as utility-scale solar projects.

There are several major competitors in the fiercely competitive High Temperature market, including First Solar, SunPower, and Trina Solar. To lower the price of high temperatures and increase the effectiveness of solar panels, these companies are continuously inventing and creating new solar technologies.

There are several anticipated advantages to the expansion of the High Temperature segment of the global proton exchange membrane fuel cell market, including

Decreased greenhouse gas emissionsOne clean energy source that doesn't emit greenhouse gases is high temperatures. This indicates that lowering greenhouse gas emissions and slowing down climate change will be aided by the expansion of the High Temperature segment of the global proton exchange membrane fuel cell market.

More funding for renewable energy projects will result from the expansion of the High Temperature segment of the global proton exchange membrane fuel cell market. This will facilitate the shift to clean energy and lessen dependency on fossil fuels.

Jobs will be created in the High Temperature industry as a result of the expansion of the High Temperature segment of the global proton exchange membrane fuel cell market. This will contribute to economic growth and open doors for people worldwide.

Regional Insights

The global market for proton exchange membrane fuel cells (PEMFCs) is dominated by the automotive industry. There are several reasons for this dominance, including

Government supportTo encourage the use of fuel cell vehicles (FCVs), governments worldwide are offering financial incentives and other types of assistance. The automotive industry's need for PEMFCs is being driven by this.

Growing demand for FCVsAs more and more buyers search for cars that are both fuel-efficient and environmentally friendly, there is a growing demand for FCVs. The automotive industry's need for PEMFCs is being driven by this.

Technological developmentsPEMFC technology has improved dramatically in the last several years, increasing the efficiency, robustness, and affordability of PEMFCs. PEMFCs are becoming more appealing for use in FCVs as a result.

The PEMFC market is expanding significantly in other segments as well, including stationary and portable. For the foreseeable future, the automotive segment is anticipated to continue to hold a dominant position in this market.

It is anticipated that the global PEMFC market for the automotive segment will keep expanding quickly in the years to come. The rising demand for FCVs and the ongoing developments in PEMFC technology will be the main drivers of this growth.

Here are some more details about the global PEMFC market's automotive segment

Passenger cars and commercial vehicles are two more subcategories of the automotive market.

With over 80% of the automotiv market, the passenger vehicle segment is the larger of the two.

Download Free Sample Ask for Discount Request Customization

A list of key players

-

Ballard Power Systems (Canada)

-

Bloom Energy (USA)

-

FuelCell Energy (USA)

-

Hydrogenics Corporation (Canada, a Cummins Inc. company)

-

Nel ASA (Norway)

Proton Exchange Membrane Fuel Cell (PEMFC) Market Scope

| Category | Segment | Description |

|---|---|---|

| By Type | High Temperature PEMFC | Operates above 120°C; suitable for CHP applications. |

| Low Temperature PEMFC | Operates below 100°C; used in transport and portable devices. | |

| By Application | Stationary | For residential, commercial, and industrial power generation. |

| Portable | Used in backup power and small electronics. | |

| Transport | Powers vehicles such as cars, buses, and trains. | |

| Others | Aerospace, military, and maritime uses. | |

| By Capacity | <1 kW | For portable and small-scale applications. |

| 1–250 kW | Residential and light commercial systems. | |

| 250–500 kW | Medium-scale industrial power systems. | |

| >500 kW | Large-scale industrial and utility generation. | |

| By Region | North America | Strong R&D support and favorable policies. |

| Europe | Driven by clean energy regulations. | |

| Asia-Pacific | Largest market with major hydrogen investments. | |

| Latin America | Emerging region with sustainability initiatives. | |

| Middle East & Africa | Growing infrastructure and government focus on hydrogen economy. |

Related Reports

FAQ'S

For a single, multi and corporate client license, the report will be available in PDF format. Sample report would be given you in excel format. For more questions please contact:

Within 24 to 48 hrs.

You can contact Sales team (sales@marketinsightsresearch.com) and they will direct you on email

You can order a report by selecting payment methods, which is bank wire or online payment through any Debit/Credit card, Razor pay or PayPal.

Discounts are available.

Hard Copy