| Forecast Period | 2024-2028 |

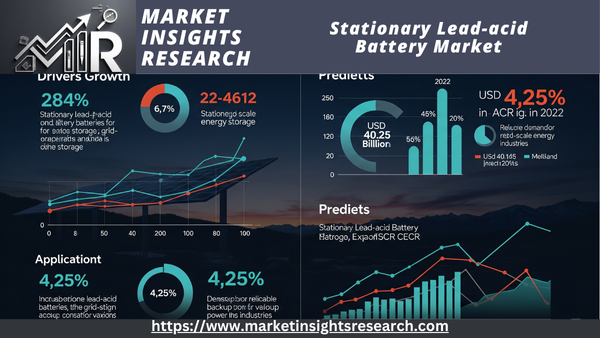

| Market Size (2022) | USD 40.25 Billion |

| CAGR (2023-2028) | 4.25% |

| Fastest Growing Segment | transportation |

| Largest Market | Asia Pacific |

Market Overview

The Global Stationary Lead-acid Battery Market reached a size of USD 40.25 billion in 2022 and is a CAGR of 4.25% from 2022 to 2028.

Download Free Sample Ask for Discount Request Customization

Key Market Drivers

One area of the clean energy sector that is concentrated on the creation, production, and application of PEM fuel cell systems is the stationary lead-acid battery market. PEM fuel cells are well-known for their low emissions, high energy efficiency, and adaptability to a range of uses, such as portable electronics, stationary power generation, and transportation. Numerous important factors impact the market's growth and development. The following are the main factors propelling the PEM fuel cell marketOne of the main factors propelling the PEM fuel cell market is the worldwide drive for sustainable and clean energy sources to lessen greenhouse gas emissions and combat climate change. PEM fuel cells are a clean energy source because they generate electricity by reacting hydrogen and oxygen chemically, with the only byproduct being water vapor. PEM fuel cells have a lot of potential in the transportation industry, especially in fuel cell electric vehicles (FCEVs). Because of the need to lower carbon emissions and enhance air quality, governments and automakers are investing in FCEV technology as an alternative to internal combustion engines. PEM fuel cells are strongly influenced by the growth of a hydrogen economy, which produces, stores, and uses hydrogen as an energy carrier. Fuel cells can effectively produce electricity by using hydrogen, which can be produced from various sources, including renewable energy. Grid-level energy storage and backup power systems are two examples of energy storage applications where PEM fuel cells can be useful. The need for reliable and effective energy storage solutions to balance sporadic renewable energy sources drives the market.

Decentralized Energy Generation

Distributed or decentralized energy generation is possible with PEM fuel cells. They work well in combined heat and power (CHP) systems, which supply homes and businesses with both heat and electricity. Investment and uptake of PEM fuel cell systems are encouraged by favorable government regulations, incentives, and subsidies meant to advance clean energy technologies, such as fuel cells.

Research and Development

Ongoing research and development initiatives are driving market developments by enhancing the performance, robustness, and affordability of PEM fuel cell technology. Market expansion is facilitated by advancements in manufacturing techniques and materials. Cooperation on hydrogen and fuel cell research and development between nations and international organizations promotes innovation and increases market potential. PEM fuel cell technology is finding uses outside of its conventional applications as it develops. This covers off-grid power generation, small-scale portable fuel cells for consumer electronics, and backup power for telecom infrastructure. PEM fuel cells are becoming more popular as a sustainable and effective energy source as a result of consumers' and businesses' growing awareness of clean energy options and environmental issues. One of the main factors propelling the use of PEM fuel cell vehicles is the development of hydrogen refueling infrastructure for FCEVs. Infrastructure spending is necessary to sustain market expansion. Prominent pilot programs and demonstration projects that highlight the advantages and capabilities of PEM fuel cell technology contribute to market acceptance and confidence-building.

Download Free Sample Ask for Discount Request Customization

Key Market Challenges

High Manufacturing Costs

The comparatively high manufacturing costs of PEM fuel cells, which are mostly caused by the use of pricey catalyst materials like platinum in the electrodes, are one of the main obstacles. We must decrease these costs to make PEM fuel cells more competitive with other energy sources. For PEM fuel cells to be profitable, they must run effectively for long stretches of time. One major challenge is ensuring the long-term durability and longevity of fuel cell components, particularly the catalysts and proton-conducting membrane. High-voltage cycling, contaminants, and fuel impurities can all have an impact on the catalysts used in PEM fuel cells. Degradation of the catalyst can have a major effect on the fuel cell's lifespan and performance. The main fuel for PEM fuel cells is hydrogen, and there are still many obstacles to overcome in terms of distribution, storage, and transportation. The expansion of the market depends on the development of economical, safe, and effective hydrogen infrastructure. One obstacle to the broad use of fuel cell vehicles is the absence of a complete infrastructure for hydrogen fueling. It takes a lot of planning and money to expand hydrogen refueling stations. The majority of hydrogen is produced using fossil fuels, which runs counter to clean energy's objective. It's difficult to create sustainable and scalable processes for producing hydrogen, like electrolysis with renewable energy. Proper water management is necessary for PEM fuel cells to avoid flooding or dehydration of the proton-conducting membrane. For the fuel cell to operate at its best, the water content must be balanced.

Cold Start and Freezing

Because of the possibility of water freezing inside the cell, PEM fuel cells can be difficult to operate in cold weather. For cold-weather applications, creating efficient insulation and heating solutions is crucial. It can be difficult to move from laboratory-scale prototypes to large-scale commercial production. For PEM fuel cell producers, ensuring consistent performance and dependability at scale is a major challenge. Because it is flammable, hydrogen is dangerous, especially when used in transportation. Public acceptance of hydrogen depends on its safe handling, storage, and use. Other clean energy technologies that compete with PEM fuel cells include solid oxide fuel cells and lithium-ion batteries. These technologies have different benefits and might be more appropriate for specific uses. Market expansion may be impeded by inconsistent fuel cell and hydrogen regulatory frameworks and policies. To encourage adoption, laws must be supportive and unambiguous. It's difficult to build public confidence and awareness of fuel cell technology. Adoption rates may be impacted by how the general public views and comprehends fuel cells, particularly when compared to more established technologies like internal combustion engines.

Despite these obstacles, many of them are being addressed by continued R&D initiatives, government assistance, and industry-academia partnerships. PEM fuel cells are anticipated to be crucial to the development of sustainable and effective energy solutions as technology develops and clean energy objectives gain importance. For the PEM fuel cell market to realize its full potential and help create a cleaner, more sustainable energy future, these obstacles must be overcome.

Key Market Trends

Government Initiatives and Growing Private Investments are Expected to Drive the Market

The introduction of government initiatives in important markets and growing private sector investment support were the primary drivers of the PEM fuel cell market's notable growth over the past two years. Long-term authority to co-fund the first 100 retail hydrogen stations was established in 2013 through the Alternative and Renewable Fuel and Vehicle Technology Program of the Californian Energy Commission, a government initiative. This incentivized the private sector to make investments in the market for fuel cells. By 2030, the California Fuel Cell Partnership hopes to have a network of 1,000 hydrogen stations and up to 1,000,000 fuel cell vehicles. More than 40 partners, including universities, government agencies, non-governmental organizations, automakers, fuel cell technology companies, and energy companies, contributed to and agreed upon the goal. High-temperature polymer electrolyte membrane fuel cells (HT-PEMFCs) are a promising option for powering heavy-duty vehicles and other large transportation needs because they can effectively manage heat, based on a project done in February 2022. Furthermore, several organizations participated in this project, including Toyota Research Institute of North America (Zhendong Hu and Hongfei Jia), LANL (Katie Lim), Sandia National Labs (Cy Fujimoto), Korea Institute of Science and Technology (Jiyoon Jung), University of New Mexico (Ivana Gonzales), and University of Connecticut (Jasna Jankovic). The PEM type is the most widely used fuel cell. It is anticipated to be a key factor in Europe's goal for fuel cell deployment and propel the market for PEM fuel cells.

Researchers at Los Alamos National Laboratory created a novel polymer fuel cell that runs at higher temperatures in February 2022. A new high-temperature polymer fuel cell that operates at 80-160 degrees Celsius and has a higher rated power density than state-of-the-art fuel cells has solved the long-standing problem of overheating, which is one of the largest technical barriers to using medium- and heavy-duty fuel cells in vehicles, such as trucks and buses. Additionally, the demand for fuel cell-based vehicles is growing globally. The two nations with the largest stocks of fuel cell-based automobiles worldwide are North Korea and the United States. North Korea and the United States accounted for 38% and 24% of the global stock of fuel cell-based vehicles in 2021, respectively. Therefore, during the forecast period, the market is expected to be driven by such government initiatives and investments. Due to the aforementioned factors, we anticipate that government programs and rising private investments in PEMFC technology will propel the market during the forecast period.

Segmental Insights

End Use Insights

The PEM fuel cell market's largest segment is the automotive industry. Growing environmental concerns and the need for cleaner and more sustainable transportation options are driving the demand for PEM fuel cells in the automotive industry. PEM fuel cells are utilized in trucks, cars, and buses that run on fuel cells. The PEM fuel cell market's second-largest segment is the industrial sector. The need for energy storage and backup power systems is driving the industrial segment's demand for PEM fuel cells. Data centers, telecommunications, and manufacturing are just a few of the industrial settings where PEM fuel cells find use.

Regional Insights

The Asia pacific region has established itself as the leader in the Global Stationary Lead-acid Battery Market with a significant revenue share in 2022

Download Free Sample Ask for Discount Request Customization

Recent Developments

- China has plans to manufacture 100,000 to 200,000 tonnes of renewable hydrogen annually and have a fleet of 50,000 hydrogen-fueled vehicles by 2025. China is currently the world's largest market for fuel-cell trucks and buses and the third-largest for fuel-cell electric vehicles (FCEVs).

- Indian Scientists have indigenously developed platinum-based electrocatalysts for fuel cells through an efficient procedure. This electrocatalyst showed comparable properties to the commercially available electrocatalyst and could enhance the lifetime of the fuel cell's performance.

- August 2022The National Renewable Energy Laboratory (NREL) began collaborating with Toyota Motor North America (Toyota) through a cooperative research and development agreement to build, install, and evaluate a 1-megawatt (MW) proton exchange membrane (PEM) fuel cell power generation system at NREL’s Flatirons Campus.

Key Market Players

- Tesla, Inc

- Panasonic Corporation

- LG Chem

- Samsung SDI

- BYD Company Limited

- CATL

- A123 Systems

- Enphase Energy

- NEC Energy Solutions

- Saft Group

|

By Technology |

By Application |

By Region |

|

|

|

Related Reports

FAQ'S

For a single, multi and corporate client license, the report will be available in PDF format. Sample report would be given you in excel format. For more questions please contact:

Within 24 to 48 hrs.

You can contact Sales team (sales@marketinsightsresearch.com) and they will direct you on email

You can order a report by selecting payment methods, which is bank wire or online payment through any Debit/Credit card, Razor pay or PayPal.

Discounts are available.

Hard Copy